How Devaluation Forced Egypt’s Online Fashion Market to Go Local. And Win.

Egypt’s online fashion market recovered to above $800M+ by 2025, surpassing pre-devaluation levels. Most observers stopped at that headline.

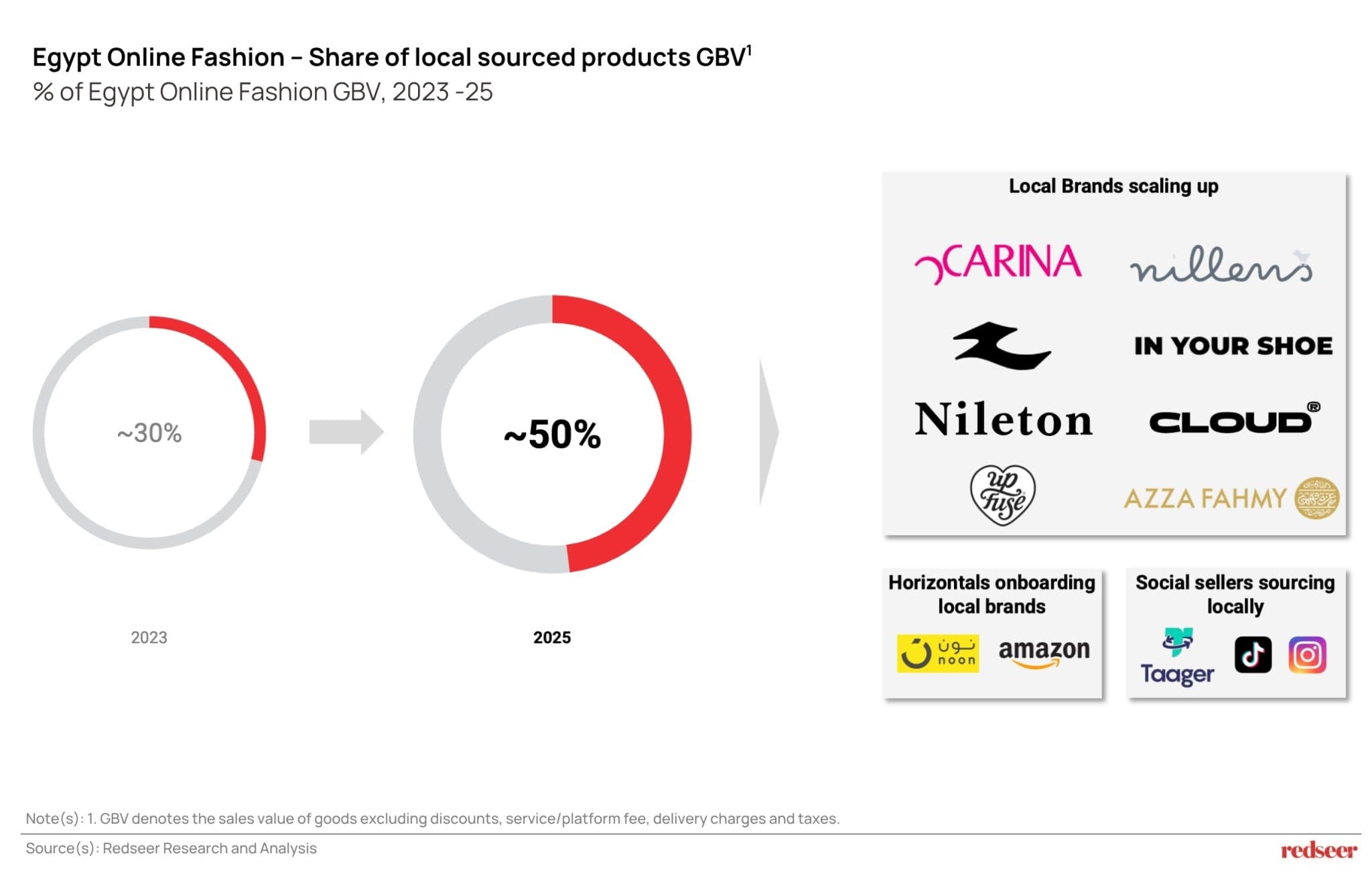

The more important number sits underneath it. Redseer estimates that locally sourced products accounted for roughly one-third of Egypt’s online fashion market in 2023. By 2025, that share had grown to approximately half. In two years, Egypt’s online fashion supply base restructured itself almost beyond recognition.

This did not happen because of a government push or a strategic pivot by global platforms. It happened because a currency shock made import-cost-dependent business models unviable almost overnight, and local alternatives were ready to fill the gap. What followed was an accidental but enduring transformation.

- ~1 in 3 products locally sourced in Egypt’s online fashion market in 2023

- ~1 in 2 products locally sourced by 2025, a structural shift, not a blip

- $800M+ market size in 2025, above pre-devaluation levels

What the Devaluation actually did

In March 2024, the Egyptian pound lost more than 60% of its value in a single adjustment. The effect on import-cost-dependent online fashion players was immediate and severe.

The business model that broke was simple to describe – buy or source in dollars, sell in Egyptian pounds. When the pound repriced, that model repriced with it. A product that had looked accessible to a price-sensitive Egyptian consumer suddenly did not. The affordability equation broke.

The players who felt this most acutely were those with the least ability to adjust their cost base quickly. Shein’s cross-border model was almost entirely exposed to the FX move. Yashry & Dresscode, operating on import-heavy inventory, faced the same pressure. All scaled back significantly. The etailing specialist segment as a whole saw its market contribution fall from ~30% to ~15%, halving in a single year.

This is not a story about international versus local. Yashry and Dresscode are Egyptian platforms. The distinction that mattered was not where a company was based out of; it was on which side of the currency divide its cost base sat.

The local ecosystem that stepped into the gap

Three things grew as the import-dependent model contracted. Each represents a different layer of Egypt’s new commercial infrastructure.

Horizontal marketplaces were the largest structural beneficiaries. Noon’s response was instructive: rather than absorb the FX exposure, they accelerated local seller onboarding. Egyptian brands producing and pricing in EGP became the growth engine for the platform. Amazon took a similar approach. Both platforms effectively converted a currency crisis into a seller recruitment opportunity, repositioning themselves as a distribution infrastructure for local supply rather than facilitators of imported inventory.

D2C and social commerce formalized at scale. More than 7,000 small Egyptian apparel brands are now selling through Shopify, Dukkan, and WooCommerce storefronts. Many built their businesses on Egyptian cotton, a material with a natural cost advantage in local production that became significantly more competitive once imports repriced. At the informal end, TikTok and Instagram sellers expanded rapidly, with full-stack social commerce enablers like Taager helping bring structure to what had previously been fragmented social selling.

Local brands moved up in preference among consumers. Digital-first labels like Zee and InYourShoe, which had been building online following before the devaluation, found that their moment arrived faster than expected, while legacy local brands like Carina and Nillens deepened their share of online sales. With import-led fast fashion out of the affordable range, consumers began preferring local alternatives. Many digital-first brands have since extended into physical retail, following the consumer rather than the other way around.

International omnichannel brands like H&M and LC Waikiki also held their ground. Their multi-channel footprint and brand equity gave them durability that pure-play import models did not have. But the more interesting trend was what sat beneath them – local brands gaining real traction for the first time.

From surviving to supplying: the near-snoring opportunity

The first phase of Egypt’s localization story was about survival. Local sourcing grew because import-dependent models broke. But the second phase, which is now beginning to take shape, is more interesting.

Import-dependent players who stayed in the market did not simply absorb the cost pressure. The smarter ones began near-shoring, shifting sourcing toward Egyptian manufacturers to bring their cost base closer to local currency. What started as a defensive move is becoming a strategic one. As Egypt’s local manufacturing ecosystem has matured and deepened, the quality and range of what can be sourced locally have improved. The near-shoring option that looked like a compromise in 2024 looks like a competitive advantage in 2026.

The implication extends beyond Egypt’s domestic market. Egypt now has a local fashion manufacturing base that is cost-competitive, increasingly quality-capable, and sitting next door to some of the highest-consumption markets in the world. GCC consumers spend significantly on fashion. GCC platforms are increasingly looking to build supply chain resilience. Egypt’s textile and apparel ecosystem, built and stress-tested through a domestic crisis, is now a credible near-shoring destination for regional demand.

This is the part of the Egypt story that tends to get missed. It is not just a market that survived a shock. It is a market that built capability through the shock, and that capability is now exportable.

What the rest of MEA should take from this

Egypt is now the most concrete example in the MEA region of what happens when import dependence meets a sustained cost shock. The mechanism in Egypt was currency. The same logic applies wherever landed costs rise sharply, whether through FX, logistics disruption, or import tariffs.

For investors, the Egypt story reframes how to think about local-market players across the region. A business priced in local currency, sourcing locally, selling to local consumers is not simply a small-market story. It is a resilience story. Egypt’s devaluation was the stress test. The companies that passed it have a moat that capital alone cannot easily replicate.

For platforms operating across MEA, the Egypt playbook is a reference point: local seller onboarding is not just a growth tactic, it is a hedge against the kind of supply disruption that Egypt experienced. Noon and Amazon did not lose Egypt. They adapted to it. The platform that can flex its seller mix toward local supply fastest when costs shift will outperform the one that cannot.

And for anyone tracking where the next near-shoring play in the region comes from, Egypt’s textile base is worth watching. A market that was forced to localize has ended up building the infrastructure that the wider region may increasingly want access to.

There is a version of this story that plays out more broadly across MEA. Egypt just ran the experiment first.

Written by

Sandeep Ganediwalla

Partner

Sandeep is the Partner with 20+ years of experience in consulting and technology. He has expertise in multiple sectors including ecommerce, technology, telecom and private equity.

Talk to me

Click-Book-Track: The Rise of New-Age Intracity Logistics Platforms in India

Indonesia’s USD 500 Bn Banking Gap: Can Digital Banks Win before Incumbents Digitize?

India’s Most Reliable Financial Cohort Is Also Its Most Underserved