Indonesia BNPL Market: Growth Meets Credit Discipline

Indonesia’s BNPL market has crossed USD 7 billion and continues to expand.

The discussion is now moving beyond merchant growth and transaction volumes. As credit books become larger and regulation becomes more active, providers will increasingly be judged on funding efficiency, underwriting quality, and portfolio performance.

The following content examines the changes shaping Indonesia’s BNPL market and the capabilities likely to matter most over the next few years.

Indonesia BNPL has crossed USD 7 billion, but funding, underwriting, and regulation will shape the next phase

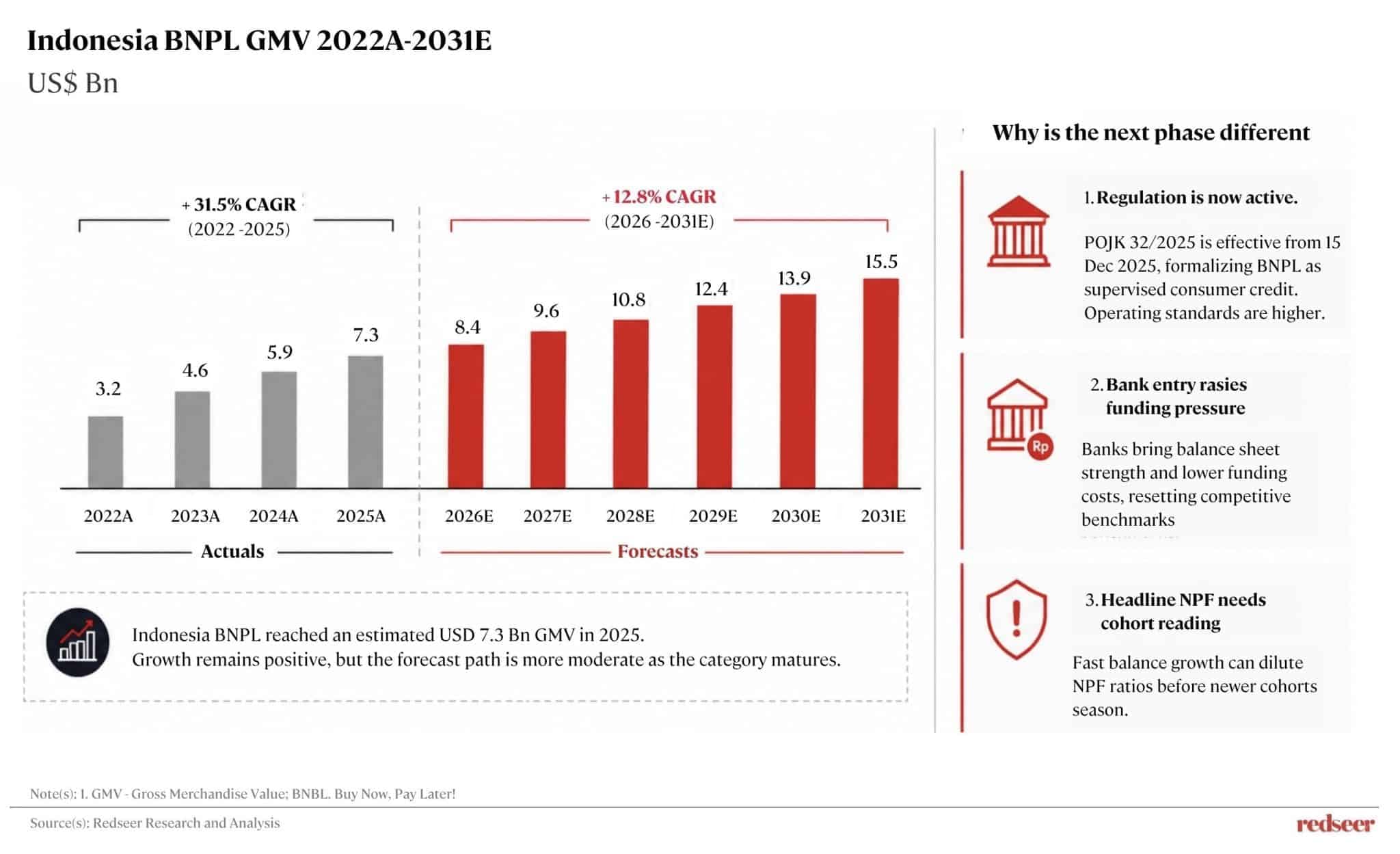

Indonesia BNPL reached USD 7.3 Bn GMV in 2025, based on our analysis. The category is still expanding, but the growth curve is becoming more measured. That is normal for a credit product moving into a regulated phase. The next stage will depend less on checkout placement and more on borrower checks, funding cost, portfolio control, and licensed issuance.

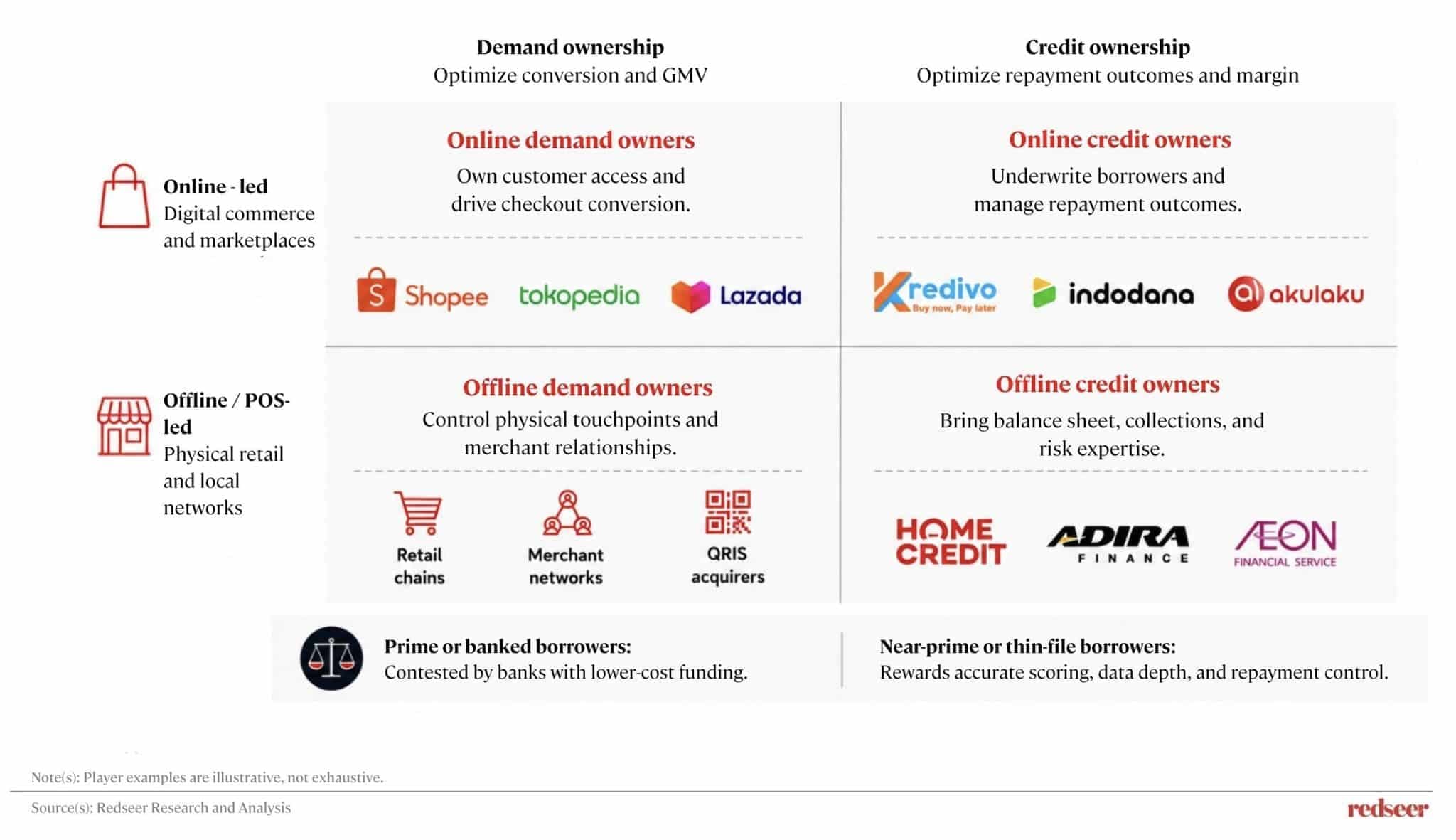

BNPL players compete on different profit equations

Indonesia’s BNPL players are optimizing for different outcomes. Marketplace-led models use BNPL to support conversion, basket size, and repeat purchases. Credit-led models need the loan book to work after funding cost, losses, and collections. That difference in goals is important as the market matures. Demand access explains who can originate. Credit discipline explains who keeps the margin.

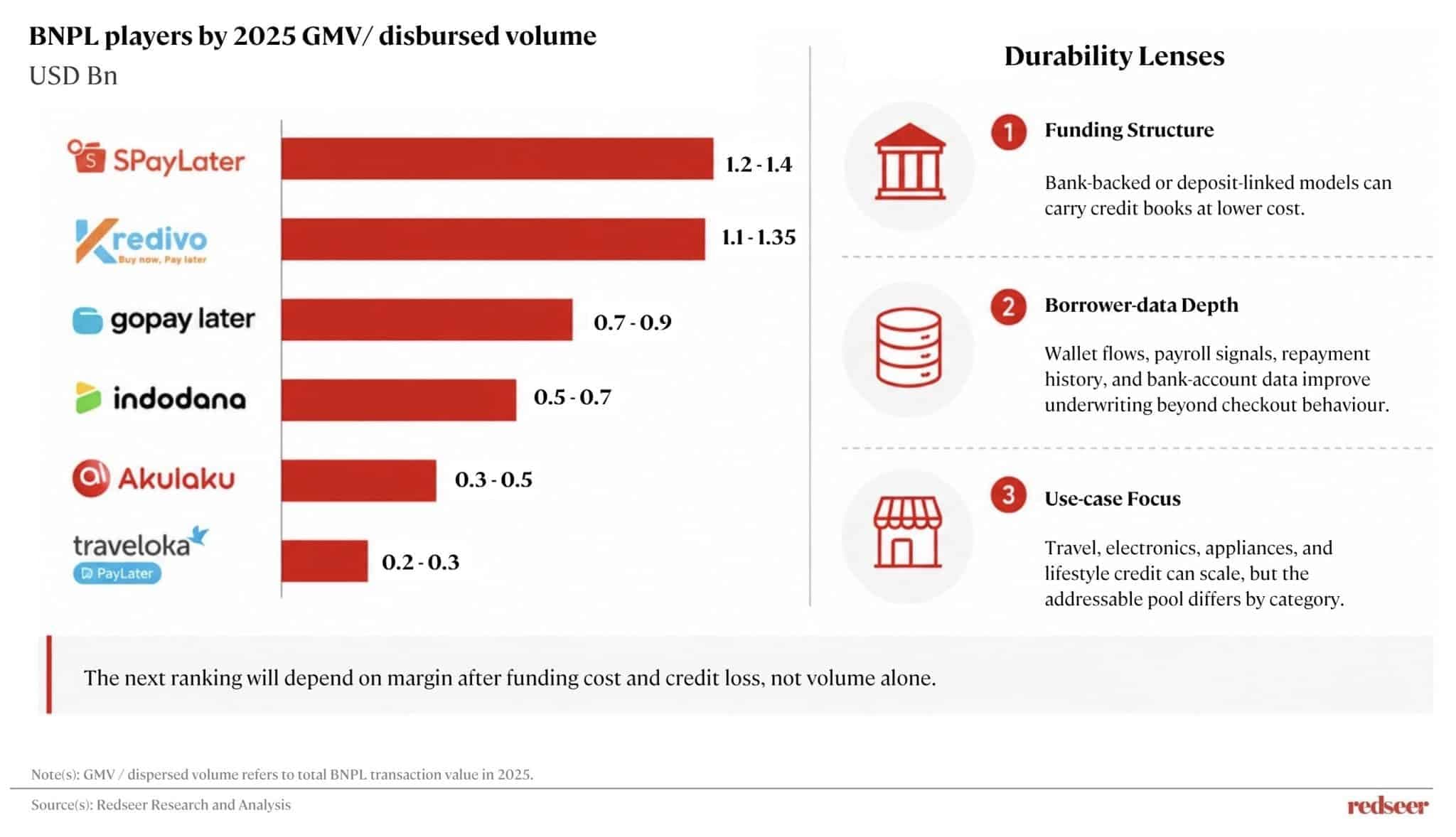

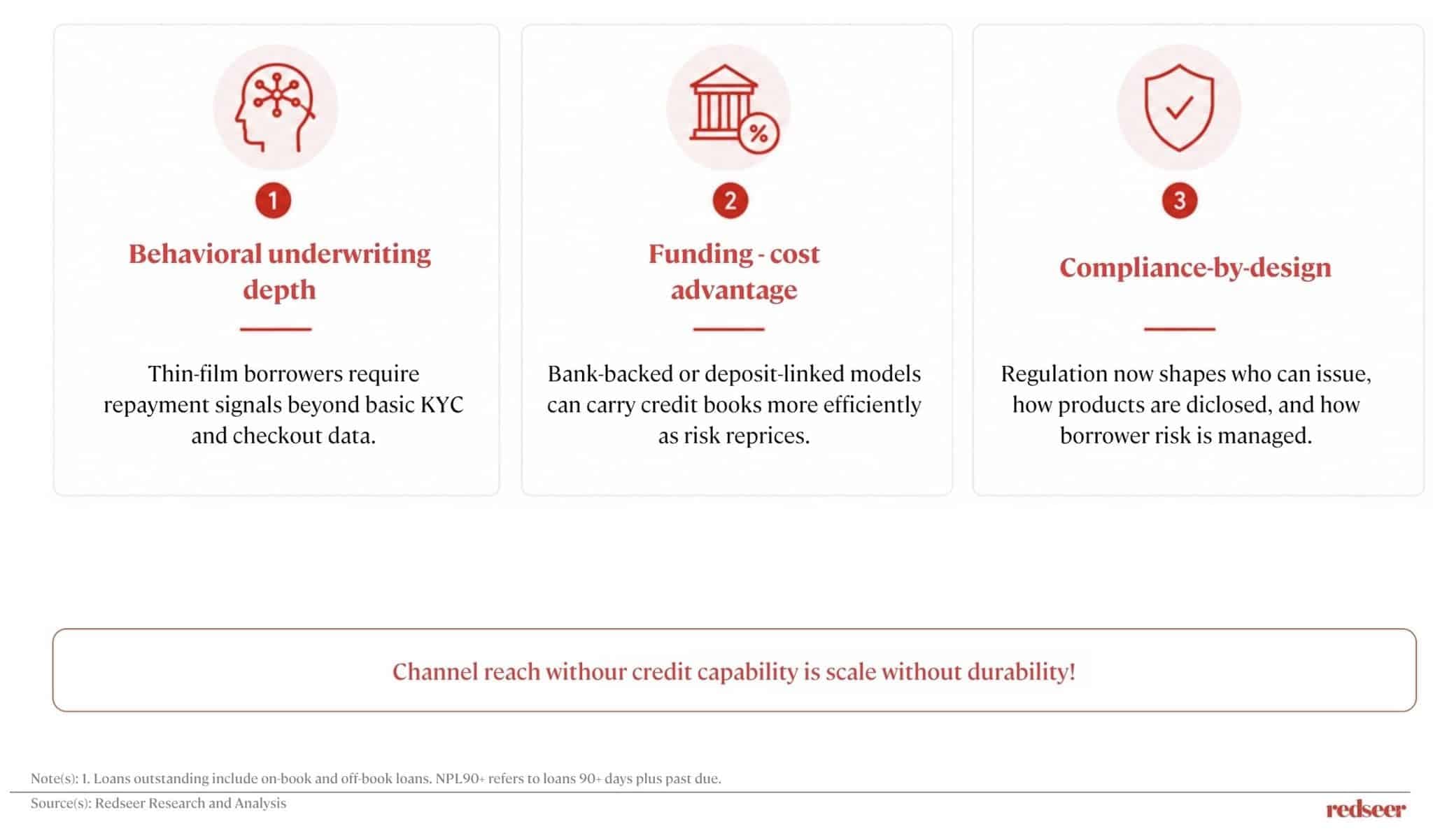

Funding cost and borrower data could matter more than GMV rank

Want to get strategic guidance?

GMV rankings show demand access. They do not show which players can sustain returns in a tighter credit cycle. Three factors will matter more over the long term: funding structure, borrower-data depth, and use- case focus. Bank-backed or deposit-linked models can carry credit books at lower cost. Better repayment and wallet signals can improve underwriting. Use cases such as travel, electronics, appliances, and lifestyle credit can scale, but each comes with a different risk profile. The next ranking will depend on margin after funding cost and credit loss, not just volume.

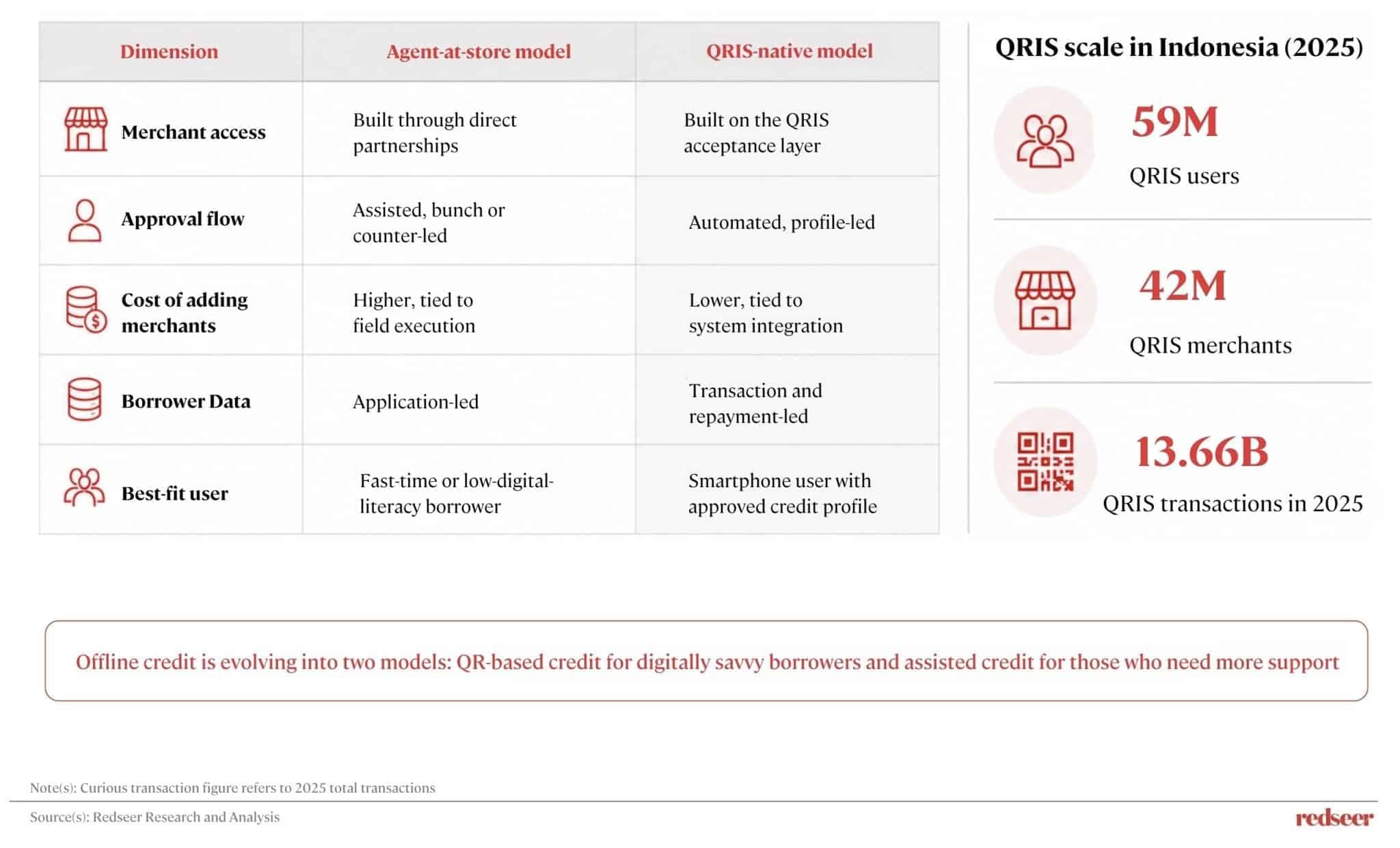

QRIS is lowering the cost of offline BNPL expansion

QRIS is changing the offline BNPL model. Traditional offline BNPL depends on merchant- by-merchant partnerships, assisted origination, and field execution. QRIS-native credit can build on a payment rail that already has national reach. That does not remove the need for assisted origination. It still matters for first-time formal- credit users, lower-digital-literacy borrowers, and higher-touch purchases. But offline credit is likely to evolve into two lanes: QR-native credit for digitally active borrowers, and assisted origination for borrowers who still need handholding.

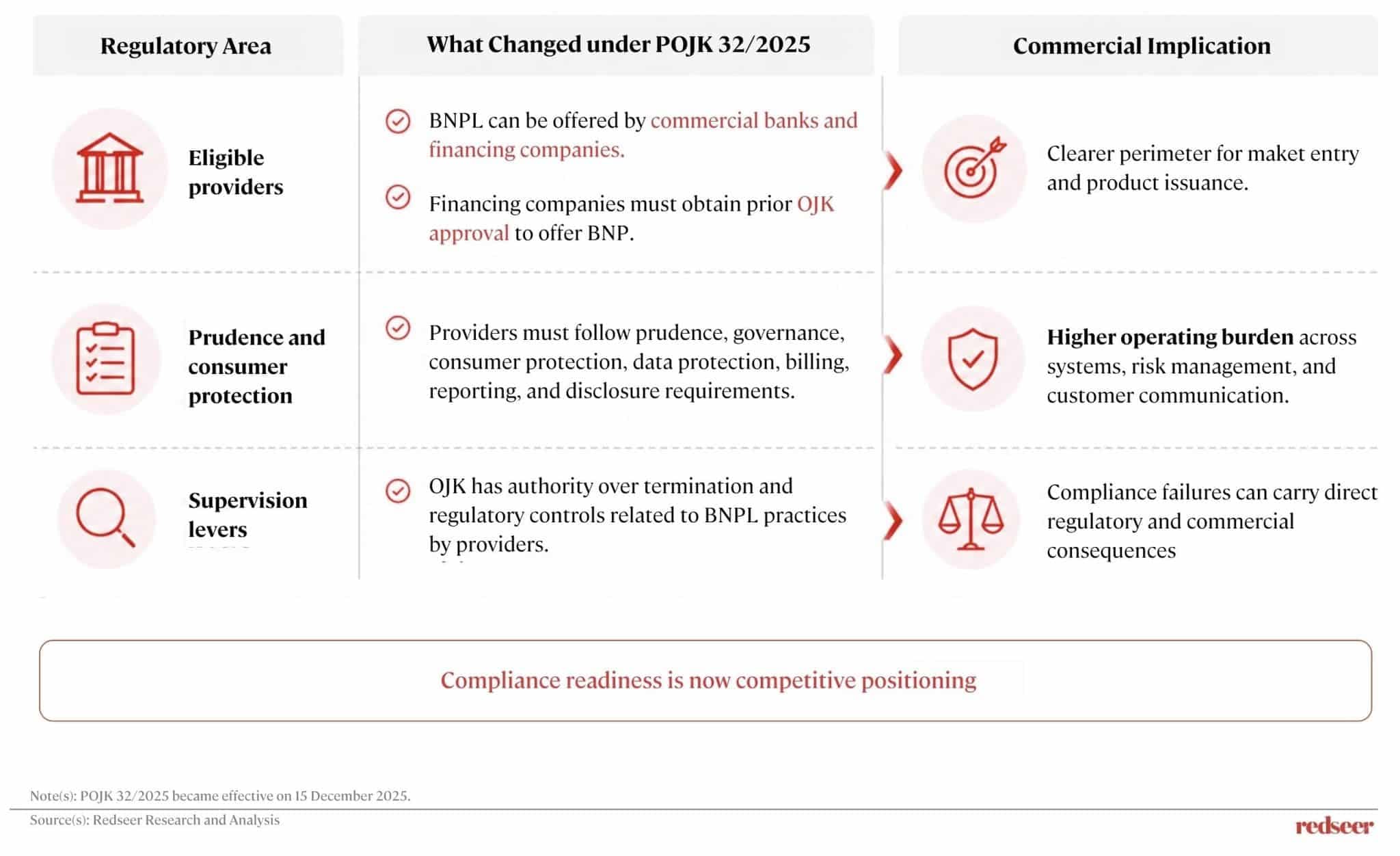

POJK 32/2025 raises the operating bar for BNPL providers

Regulation is now part of the BNPL product, moving beyond being just a back-office matter. POJK 32/2025 formalizes BNPL as supervised consumer credit. Commercial banks and financing companies can offer BNPL, while financing companies need prior OJK approval. The regulation raises the bar on prudence, governance, consumer protection, data protection, billing, reporting, and disclosure. That changes the operating model. Compliance now affects product design, borrower communication, partner trust, and the ability to keep issuing credit.

Driving Indonesia’s BNPL market from checkout-led growth to credit-led execution

Indonesia’s BNPL market has entered a phase where credit economics matter more than checkout access. Funding cost, borrower quality, portfolio performance, and regulatory execution are becoming more important as providers build larger credit books. These factors will increasingly determine which businesses convert scale into sustainable returns. Growth opportunities remain substantial, but the next stage of competition will be shaped less by distribution and more by disciplined lending.

Written by

Roshan Behera

Partner

Roshan is a Partner based in Singapore and focuses on Southeast Asia. His sector coverage includes e-commerce, logistics, fintech, eB2B, on-demand services, and other emerging sectors.

Talk to me

Viet-Nomics: Southeast Asias Rising Economic Star

USD 30 Bn Market in Motion: New Revenue Models Shaping Mobility & Delivery in SEA

The $6 Tn Question: Who Wins SEA’s Digital Payment War?

Indonesia’s USD 500 Bn Banking Gap: Can Digital Banks Win before Incumbents Digitize?

SEA BNPL: Superior Unit Economics Powering Sustainable Growth

Quick Commerce: Winning SEA through Categories, Channels and Occasions

SEA’s USD 123 Bn Remittance Market: Fragmented Landscape, Focused Winners

Indonesia’s Digital Banks Are Coming of Age:Can Incumbents Fight Back?

SEA POS: Monetizing beyond the USD 680 Bn opportunity at checkout

Southeast Asia’s Next Unicorn Factory: The $480B MSME Lending Market

2025: The Mean Matters

Rewriting the Recipe: Why Healthier Snacks Are Gaining Ground in Indonesia

Viet-Nomics: Southeast Asias Rising Economic Star

USD 30 Bn Market in Motion: New Revenue Models Shaping Mobility & Delivery in SEA

The $6 Tn Question: Who Wins SEA’s Digital Payment War?

Indonesia’s USD 500 Bn Banking Gap: Can Digital Banks Win before Incumbents Digitize?

SEA BNPL: Superior Unit Economics Powering Sustainable Growth

Quick Commerce: Winning SEA through Categories, Channels and Occasions

SEA’s USD 123 Bn Remittance Market: Fragmented Landscape, Focused Winners

Related Redsights

Viet-Nomics: Southeast Asias Rising Economic Star

USD 30 Bn Market in Motion: New Revenue Models Shaping Mobility & Delivery in SEA

The $6 Tn Question: Who Wins SEA’s Digital Payment War?

Indonesia’s USD 500 Bn Banking Gap: Can Digital Banks Win before Incumbents Digitize?

SEA BNPL: Superior Unit Economics Powering Sustainable Growth

Quick Commerce: Winning SEA through Categories, Channels and Occasions

SEA’s USD 123 Bn Remittance Market: Fragmented Landscape, Focused Winners

Indonesia’s Digital Banks Are Coming of Age:Can Incumbents Fight Back?

SEA POS: Monetizing beyond the USD 680 Bn opportunity at checkout

Southeast Asia’s Next Unicorn Factory: The $480B MSME Lending Market

2025: The Mean Matters