The customer is still human. The agent is not.

The buyer has changed. The playbook hasn’t.

Somewhere between a product query on an AI assistant and an automated reorder triggered without any human input, the advertising industry’s most basic premise is shifting. The funnel was always designed around a person at the end of it – someone who could be reached, nudged, wowed, and converted. That person is increasingly using an agent to buy: a system that researches, compares and transacts on their behalf, with no interest in creative, no loyalty to brands and no patience for mid-funnel persuasion. Redseer’s May 2026 report on AI and advertising puts a number on how fast that is changing.

By 2030, agentic commerce is expected to intermediate 10-25% of US e-commerce sales, a scale that makes this not a fringe shift but a structural one. The global advertising market hit $1.056 Tn in 2025, already growing faster than global GDP, with ad spend as a share of GDP rising from 0.6% in 2015 to 0.9% in 2025. 76% of it is digital, with 80-85% of that digital spend flowing through programmatic channels and every dollar of it was built to influence human behaviour. The human still wants the product; what has changed is that an agent, not a person, now executes the purchase decision and it does not respond to the same signals.

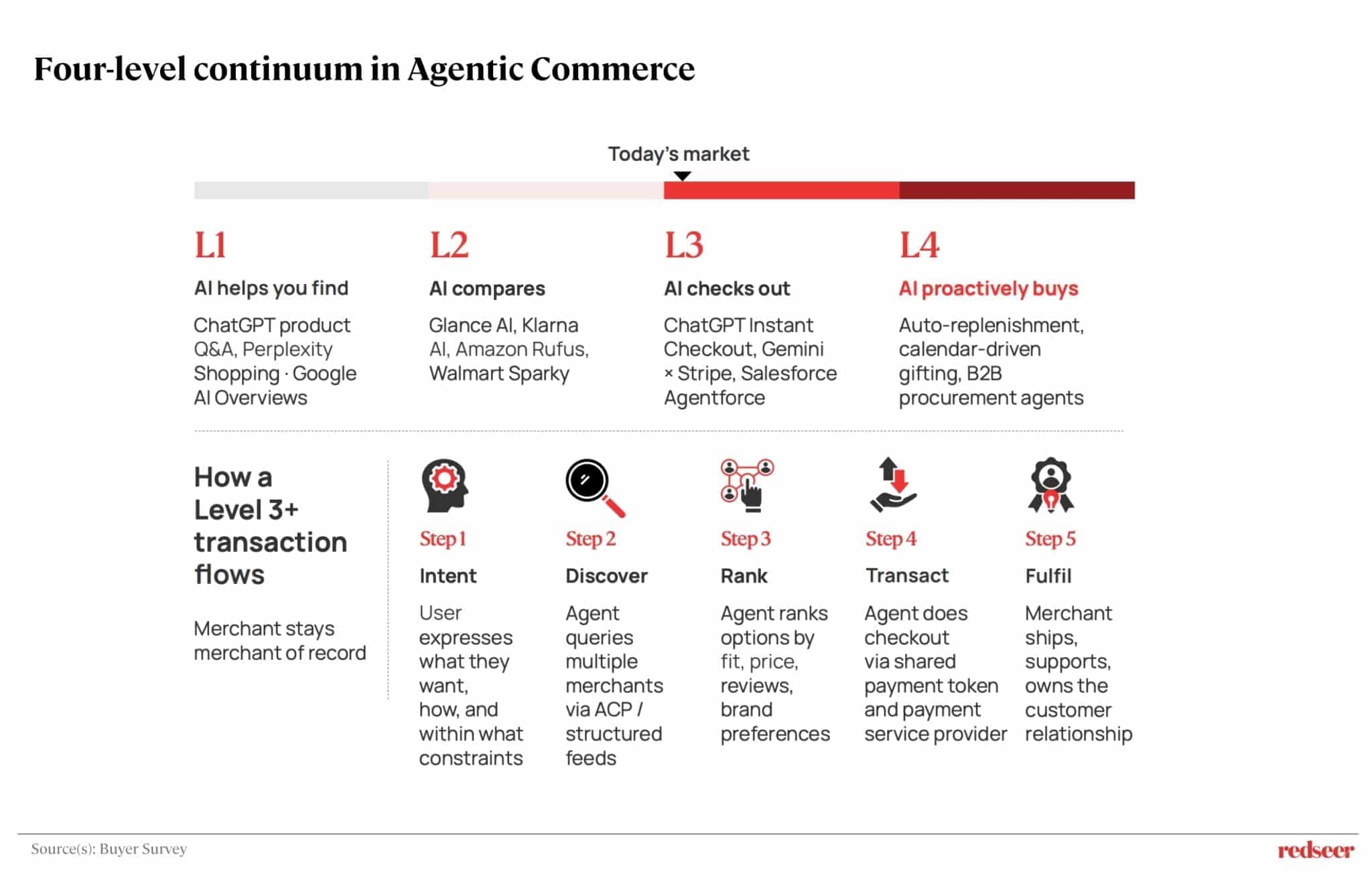

From ‘AI helps you find’ to ‘AI proactively buys’

The shift is not happening all at once. The report arranges agentic commerce across four levels of involvement. At Level 1, AI helps consumers find – purchasing-related queries that already account for 6-10% of all ChatGPT usage today, alongside Perplexity Shopping and Google AI Overviews. At Level 2, it compares – Glance AI (8 Mn+ monthly users in the US as of early 2026), Amazon Rufus, and Walmart Sparky are already live. At Level 3, AI checks out: ChatGPT Instant Checkout powered by the Agentic Commerce Protocol (ACP) and Gemini integrated with Stripe are live. At Level 4, AI proactively buys – auto-replenishment, calendar-driven gifting, and B2B procurement agents that trigger purchases with no human input. Today’s market sits predominantly at Levels 1 and 2, with the 10-25% mediation figure representing the trajectory once Levels 3 and 4 reach scale.

“ChatGPT’s ad pilot in March 2026, connecting 17,000 advertisers and $1 Tn in annual commerce sales to the platform in weeks”

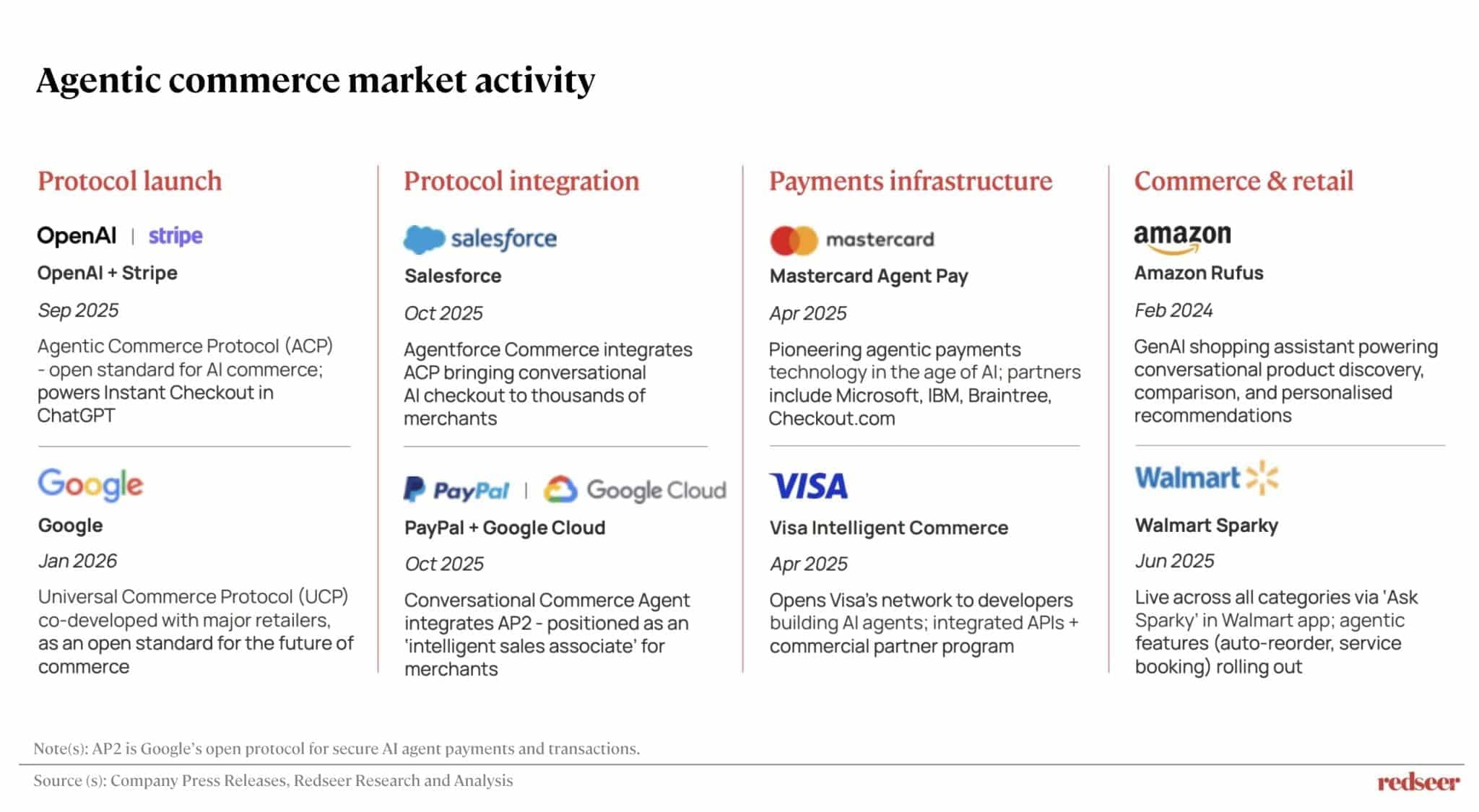

The protocol and payments infrastructure enabling that trajectory was assembled in under 18 months. Mastercard launched Agent Pay in April 2025, Visa Intelligent Commerce followed the same month, Salesforce integrated ACP in October 2025 and Google co-developed a Universal Commerce Protocol with major retailers in January 2026. When Criteo became the first AdTech partner in ChatGPT’s ad pilot in March 2026, connecting 17,000 advertisers and $1 Tn in annual commerce sales to the platform in weeks, it cemented that the route from agentic infrastructure to advertising monetization can move faster than most brands expect.

Banner ads, loyalty points and demographics are fading: here is what takes their place

The 30-year build of programmatic advertising compounded four capabilities – targeting precision, automation (auctions clearing in under 300 milliseconds), closed-loop measurement, and creative iteration speed, all built to influence a human. The $799 Bn in digital ad spend flowing through this stack today reflects that design. Agents are now executing purchases on behalf of humans within this system, and they do not share the behaviours that the stack was optimized for.

On the customer side, automated shopping assistants are completely changing how products are found and bought, making traditional marketing tactics obsolete. Visual ads and catchy headlines don’t matter to software because these assistants look at raw product data rather than creative imagery. Targeting people by age, gender, or lifestyle also becomes irrelevant since agents buy based on strict rules like maximum price and delivery speed. Standard loyalty perks can’t compete when agents can instantly find a slightly cheaper alternative elsewhere, and automated buyers can’t be chased around the internet with retargeting ads by seeing a brand over and over again.

On the selling side, the trend moves in the opposite direction. Media companies and publishers with direct, first-party relationships with their audience are becoming incredibly valuable, with some already seeing their ad inventory sell for more than x2 price of standard third-party web data.

Because of this shift, businesses need an entirely new set of strategies to get noticed and chosen. Brand trust is no longer about expensive awareness campaigns; instead, software ranks products by analyzing concrete data like customer review scores, return rates, and trust metrics. A strong brand wins because its track record is verifiably better, not because it spent the most on advertising. Furthermore, having clean, highly detailed and structured product information is the primary way a shopping assistant can find a product in the first place, giving a massive advantage to brands with superior data feeds. Finally, because software compares prices at the exact millisecond of purchase, brands that can instantly share accurate, real-time pricing through open digital channels will win the sale, while those that can’t will lose out regardless of their past reputation.

“Businesses need an entirely new set of strategies to get noticed and chosen”

Capabilities every brand needs before the window closes

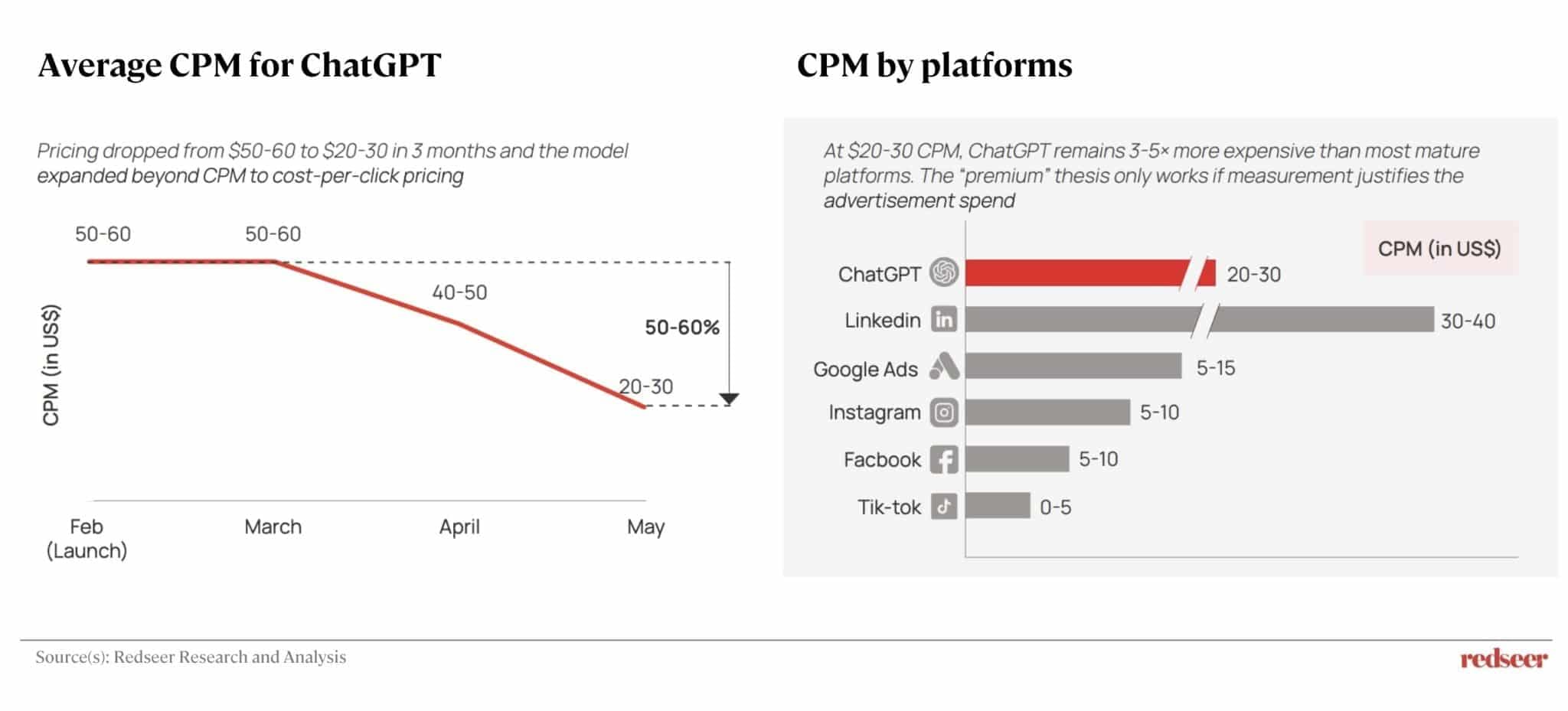

The pricing window on agent-native advertising surfaces is open right now, but it will not stay that way. ChatGPT’s average CPM fell from $50-60 at launch in February 2026 to $20-30 by May 2026, and even at that level it runs 3-5x more expensive than Facebook or TikTok, meaning the premium is only justified if measurement catches up. The OpenAI-Criteo deal shows what early movement looks like: by plugging into Criteo’s existing advertiser network rather than building its own stack, OpenAI reached meaningful scale in weeks, with LLM-referred users converting at 1.5x the rate of other channels.

The second capability is product feed quality treated as a creative asset. Structured product data – accurate pricing, inventory levels, reviews, attributes, and delivery signals – determines whether a brand is ranked or invisible when an agent queries across merchants, and AI-powered ad buying is already delivering 20-30% ROAS uplift for brands that invest in clean, structured inputs. Richer, more accurate data produces better placement, more agent-mediated transactions, and continuously improving models. .

Building on the core proposition that an open programmatic ecosystem delivers benefits when agents take over buying operations, brands that adopt the ACP, UCP, or MCP protocol have their transaction pricing cross-checked and benchmarked by agents in real time at the point of transaction. This allows these brands to gain systematic transaction advantages across all agent-mediated procurement. Brands that fail to adopt these protocols will lose the corresponding transactions, no matter how much budget they invest in exposure and brand awareness building.

“AI-powered ad buying is already delivering 20-30% ROAS uplift for brands”

Why the open programmatic ecosystem gains as agents take over buying

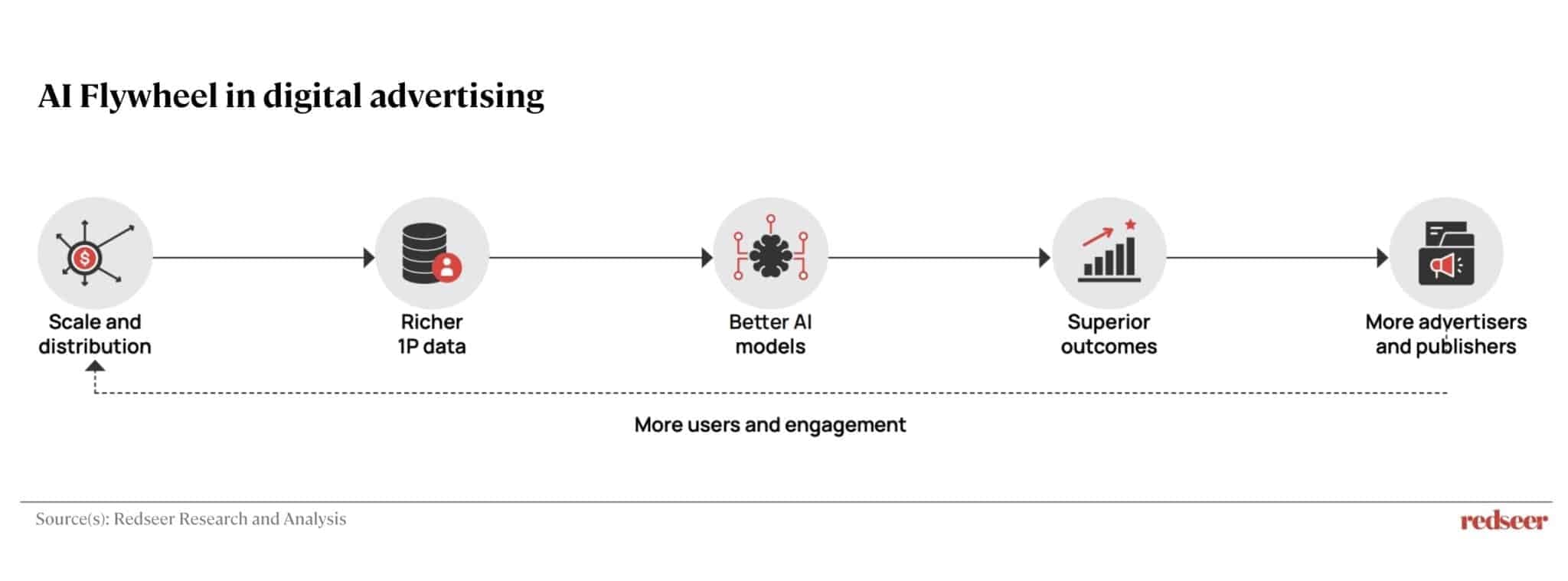

The instinctive read is that agentic commerce threatens the advertising ecosystem, but Redseer’s analysis points in the opposite direction. AI-native platforms cannot build full advertising infrastructure in-house – it takes 5-10 years and requires bidder technology, attribution, measurement, and advertiser relationships they do not have, so they will partner with the open ecosystem rather than compete with it. The surfaces they bring are substantial: time spent on GenAI apps surged from 2-3 Bn hours in 2022 to 47-49 Bn hours by 2025, a roughly 20x jump in three years, representing attention that did not exist as an advertising surface before and will not be monetized by platforms building their own stacks. The open ecosystem is the infrastructure layer that monetises the shift.

The bigger risk is to individual brands that treat this as a future problem.

Early investors in first-party data, AI-ready product feeds and agent-native surfaces generate better outcomes, attract more transactions, produce more data and train better models, widening their lead automatically. The gap between AI-mature and AI-laggard advertisers was already compounding by 2025, and in agentic commerce, where every purchase decision runs through a structured data comparison rather than a human responding to an impression, it does not narrow. It compounds.

The buyer is still human. The buying is not. The brands that adapt their playbook to that reality, rather than waiting for it to pass, are the ones that will still be winning in 2030.

Written by

Mukesh Kumar

Associate Partner

Mukesh is a go-getter with an analytical approach who enjoys solving challenging business issues. He has worked extensively in the retail, TMT, public policy, and private equity sectors and specialises in research and growth initiatives.

Talk to me

Artificial Intelligence: The Next Growth Catalyst in Advertising

Advertising Is the Oil Powering The Digital Economy

Micro-Drama’s J-Curve Moment: What Marketers, Platforms, and Investors Need to Know

Winning the Quick-Commerce Decade: Playbook for Brand Success

We enabled a leading e-commerce player with decision-grade intelligence on India’s online grocery market

Redseer enabled a leading Indian fashion marketplace to harden seller experience as a strategic moat

The internet’s most expensive mismatch

India’s leading e-commerce players’ growth execution strengthened by strategy consulting

Insights from our consulting on India’s leading conversational engagement platform scale-up journey

From Staffing the Stack to Owning It: India’s Calculated AdTech Move.

BigBasket’s business growth enabled by Redseer Consulting

Your Next High-Paying Consumer Isn’t Scrolling. They’re Living Here

Artificial Intelligence: The Next Growth Catalyst in Advertising

Advertising Is the Oil Powering The Digital Economy

Micro-Drama’s J-Curve Moment: What Marketers, Platforms, and Investors Need to Know

Winning the Quick-Commerce Decade: Playbook for Brand Success

We enabled a leading e-commerce player with decision-grade intelligence on India’s online grocery market

Redseer enabled a leading Indian fashion marketplace to harden seller experience as a strategic moat

The internet’s most expensive mismatch

Related Redsights

Artificial Intelligence: The Next Growth Catalyst in Advertising

Advertising Is the Oil Powering The Digital Economy

Micro-Drama’s J-Curve Moment: What Marketers, Platforms, and Investors Need to Know

Winning the Quick-Commerce Decade: Playbook for Brand Success

We enabled a leading e-commerce player with decision-grade intelligence on India’s online grocery market

Redseer enabled a leading Indian fashion marketplace to harden seller experience as a strategic moat

The internet’s most expensive mismatch

India’s leading e-commerce players’ growth execution strengthened by strategy consulting

Insights from our consulting on India’s leading conversational engagement platform scale-up journey

From Staffing the Stack to Owning It: India’s Calculated AdTech Move.

BigBasket’s business growth enabled by Redseer Consulting