The KSA Beauty Shelf Is Getting Crowded From Two Sides. Brand Equity Alone Won’t Hold It.

KSA’s online beauty and personal care market is one of the most attractive in the region. But the competitive ground underneath it is shifting faster than the headline growth suggests.

For years, the way to win online BPC in Saudi was reasonably settled. Global brands had the equity, the recognition, and the shelf. That position is now being squeezed from two directions at once. Cross-border players hold a strong share of sales on assortment and access, and are now setting up locally to defend it. Platforms are building their own private labels, which account for a meaningful share of sales. And the consumer caught in the middle, the one doing the buying, is changing in a way that rewards both of those pressures rather than the incumbents.

The result is simple to state. Holding position in KSA BPC is no longer about defending a brand. It is about solutioning for what the local market actually wants.

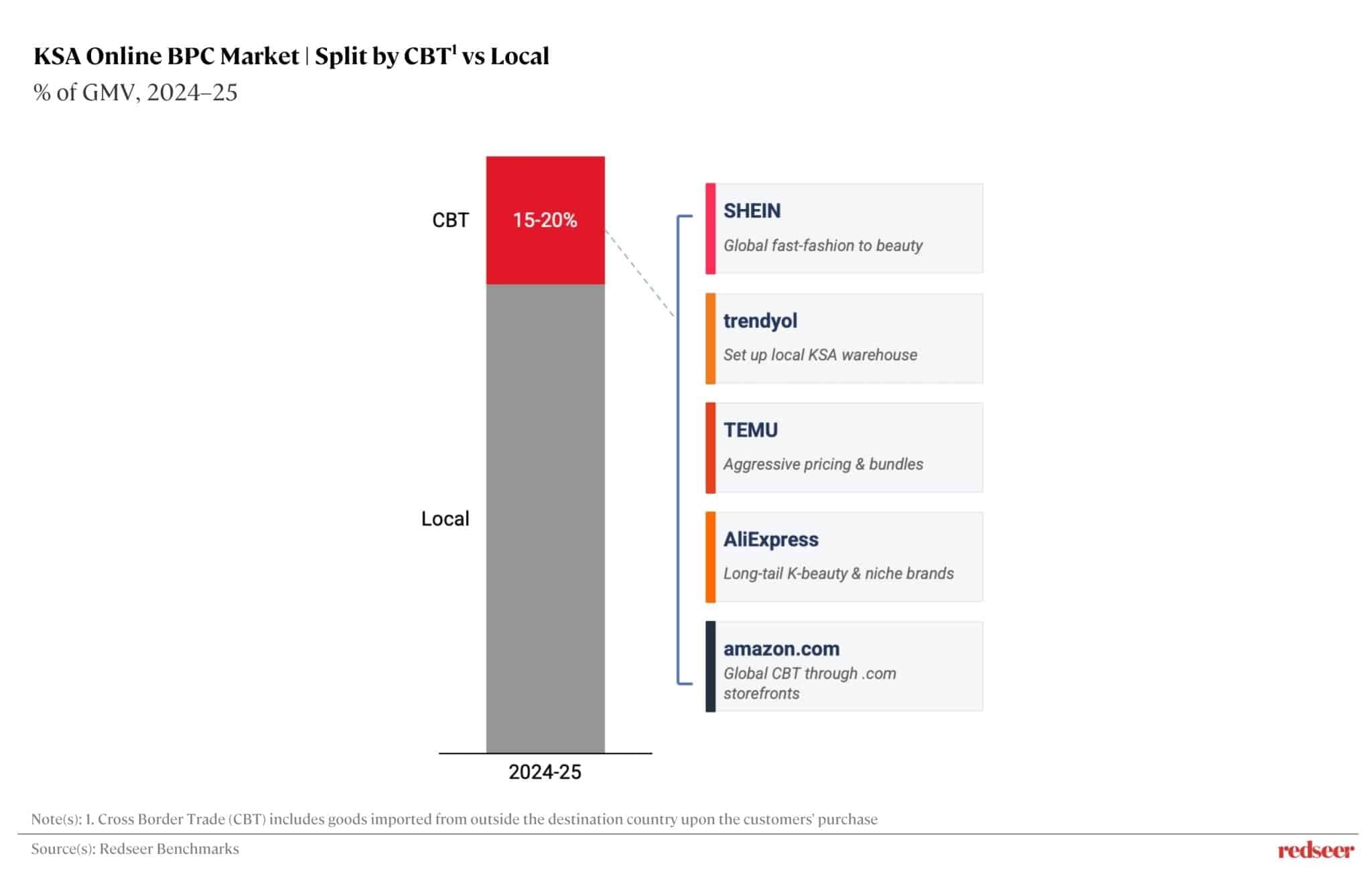

~15-20% of KSA online BPC sales come through cross-border trade

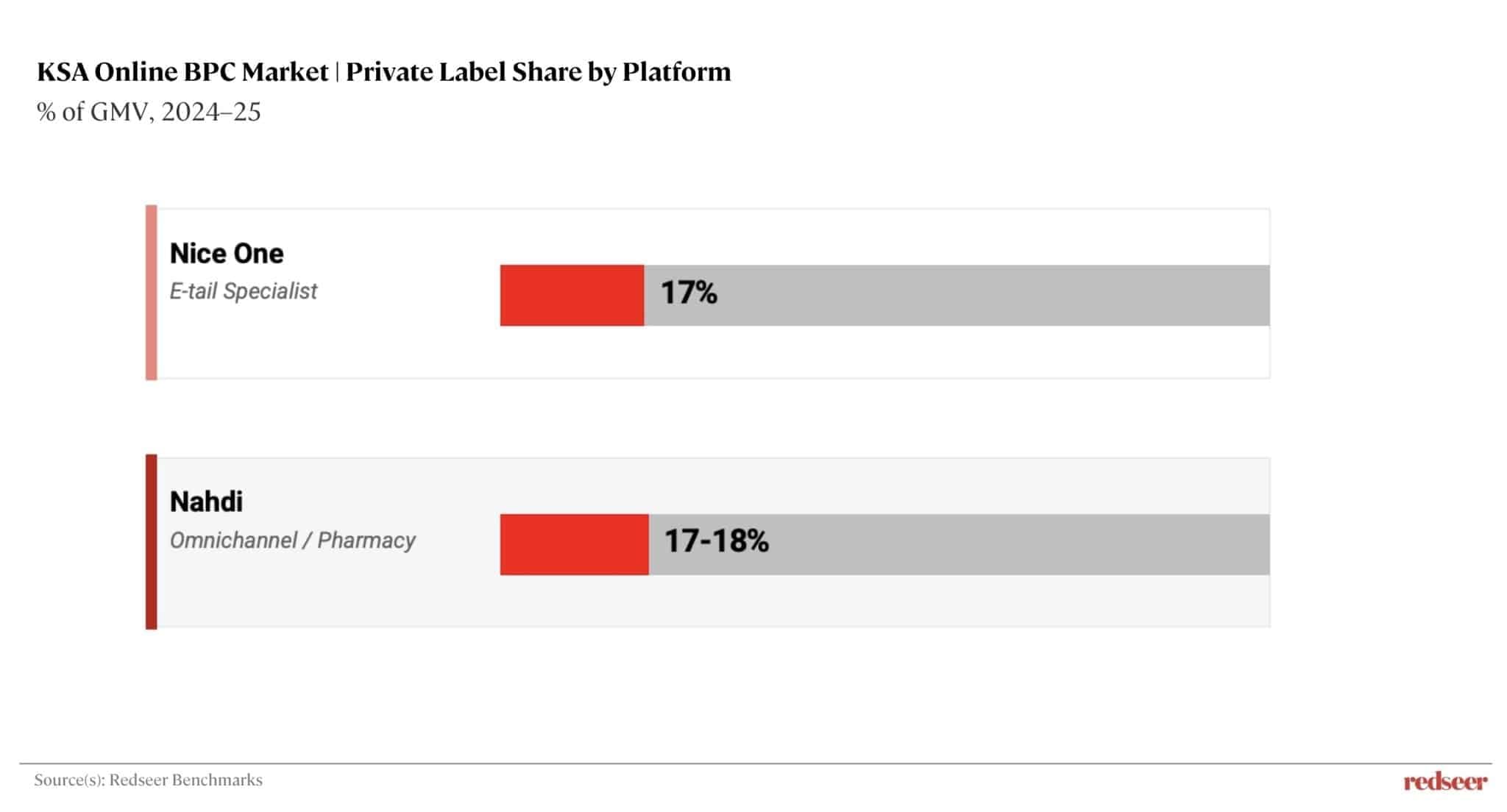

~17-20% private label share already reached by leading platforms

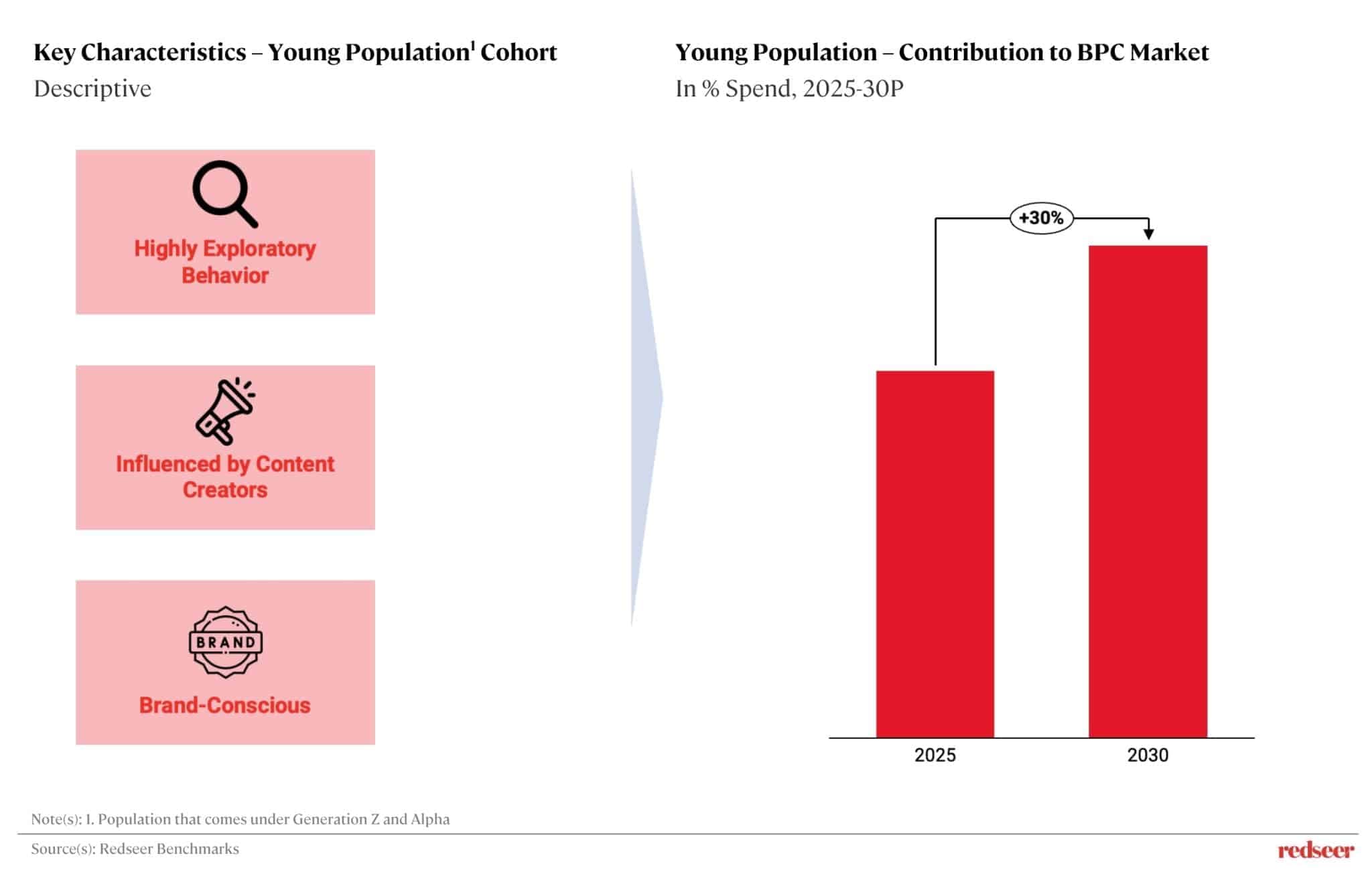

Majority of BPC spend set to come from the young cohort by 2030

Cross-border is strong, and players are now setting up locally

Cross-border trade drives 15-20% of KSA online BPC sales, led by Shein, Trendyol, Temu, AliExpress, and Amazon’s global storefronts. This is not a fringe channel. BPC is the second largest cross-border category after fashion.

The reason it holds this share is straightforward. Cross-border gives consumers access to things the local market does not stock well. Skincare and dermo-cosmetics, K-beauty, long-tail international brands, niche makeup, fragrances, shade extensions, and limited editions. For a shopper looking for a specific product rather than whatever is on the local shelf, cross-border is often the only place to find it.

The one weakness cross-border always had was speed. Local players could deliver faster, and that gap is the reason pure cross-border share has come off its peak over the years. The response from the cross-border players has been to close that gap rather than cede it. Trendyol has set up a local warehouse in KSA to localize fulfilment and match local delivery speeds. Noon and Amazon have brought global assortment into the region through their own .com storefronts. Cross-border is not retreating. It is putting down local roots, which makes its hold on assortment and access more durable.

Private label is rising, and it is reshaping the platform economics

The second pressure comes from inside the platforms themselves. Private label is growing fast across KSA online BPC, and it is concentrated among the players with the most direct reach to the consumer.

Nice One has built around 17% of sales from its own brands, spanning makeup, care, and perfumes. Nahdi has reached 17 to 18% private label share, with strong recent growth and a stated focus on beauty. Darl Amirat leads private label penetration in KSA BPC, well ahead of peers. Al Dawaa has seen its house brands grow more than 20%, with beauty and baby called out as the fastest segments.

What matters is not just the share; it is the economics. Private label typically carries better margins for platforms, and those margins help fund the broader discounting that keeps platforms competitive. For global brands, the practical effect is twofold. Private label takes up more of the shelf as it grows, and the price bar on the category moves as platforms invest in value.

Not every brand is equally exposed. Private label is hardest to replicate where brand heritage and clinical credentialing genuinely matter, so premium and dermo-cosmetic brands are more insulated. The most exposed are mass and mid-market brands sitting at the same price point, in the same channel, on the same digital shelf as the private label products being launched against them.

The consumer underneath is changing, and that is what brands need to solve for

Both pressures point at the same underlying shift. The KSA beauty consumer is getting younger, and the young cohort is set to drive the majority of BPC spend by 2030. This is the consumer, brands now must win, and they behave differently from the shopper the old playbook was built for.

Three things define them, and each one tells a brand what to do.

They are highly exploratory. They are eager to try new brands and products, and willing to switch to find the best fit. For a brand, this means equity alone holds nothing. You earn the basket each time. That puts a premium on being genuinely available and relevant, which means local fulfilment that matches cross-border on speed and an assortment that includes the niche and long-tail products people currently go cross-border to find.

They are influenced by content creators. They are digitally savvy and lean heavily on online research, creators, reviews, and tutorials before buying. Discovery has moved off the shelf and into content. Brands that are not building a credible creator and content presence lose the consideration stage before price even enters the conversation.

They are brand-conscious in a specific way. They value brand image, story, and the values a brand stands for, not just the name. This is exactly where a credible local story beats a globally translated one. It is also why homegrown KSA brands are finding an opening, and why private label can punch above its price point. Heritage on its own is not enough.

What this means for brands and platforms

Put the three pressures together, and the picture is clear. Cross-border is taking the access advantage. Private label is taking the price advantage. And the fastest-growing consumer is the one least loyal to legacy names. For incumbent global brands, the answer is not to defend the brand harder. It is to solve for local needs across the board, faster local fulfilment, local and long-tail assortment, sharper local price-points, a real content and creator presence, and a brand story that actually resonates with a young, values-driven consumer.

KSA online BPC is moving from a market where global brand equity was enough to one where local solutioning decides who holds share. The market is not getting less attractive. It is getting more contested. And the way to win it is changing in front of everyone.

Written by

Akshay Jayaprakasan

Associate Partner

Akshay brings over a decade of experience across consulting and technology, with deep exposure to India, Southeast Asia and the Middle East. He has delivered multiple keynotes, served on industry panels, and is frequently quoted by leading Middle East media on the digital economy.

Talk to me

Unlocking the Next Wave of MENA E-commerce Growth

The Two-Hour Window: How Quick Delivery is Reshaping KSA’s Beauty Market

Omnichannel Owns a Big Slice of Online Retail in KSA

The Private Label Playbook is Moving from Retail Shelves to Dark Stores

UAE Online Grocery: Dark Stores Have the Momentum. Retailers Still Have the Market.

‘Quick’ Emerging as a Growth lever for Online BPC in KSA

36% Growth. Falling Profits. Compressed Valuations. What Changed in KSA Food Delivery in 2025?

KSA is the Online Fashion & BPC leader in GCC

GCC’s Online Retail Market is Truly Democratic

Three Consumer Shifts Shaping MENA’s Demand Landscape in 2025

Dark Stores Can Be Profitable. GCC Is Where It Happens First.

UAE Ramadan 2026: Steady mood, sharper channel choices, and community-led influence

Unlocking the Next Wave of MENA E-commerce Growth

The Two-Hour Window: How Quick Delivery is Reshaping KSA’s Beauty Market

Omnichannel Owns a Big Slice of Online Retail in KSA

The Private Label Playbook is Moving from Retail Shelves to Dark Stores

UAE Online Grocery: Dark Stores Have the Momentum. Retailers Still Have the Market.

‘Quick’ Emerging as a Growth lever for Online BPC in KSA

36% Growth. Falling Profits. Compressed Valuations. What Changed in KSA Food Delivery in 2025?

Related Redsights

Unlocking the Next Wave of MENA E-commerce Growth

The Two-Hour Window: How Quick Delivery is Reshaping KSA’s Beauty Market

Omnichannel Owns a Big Slice of Online Retail in KSA

The Private Label Playbook is Moving from Retail Shelves to Dark Stores

UAE Online Grocery: Dark Stores Have the Momentum. Retailers Still Have the Market.

‘Quick’ Emerging as a Growth lever for Online BPC in KSA

36% Growth. Falling Profits. Compressed Valuations. What Changed in KSA Food Delivery in 2025?

KSA is the Online Fashion & BPC leader in GCC

GCC’s Online Retail Market is Truly Democratic

Three Consumer Shifts Shaping MENA’s Demand Landscape in 2025

Dark Stores Can Be Profitable. GCC Is Where It Happens First.