The Two-Hour Window: How Quick Delivery is Reshaping KSA’s Beauty Market

There’s a quiet but consequential shift happening in how Saudi consumers buy beauty products. It doesn’t show up loudly in headline GMV numbers, but it’s reshaping which brands win, which platforms matter, and what “being available” actually means in 2025.

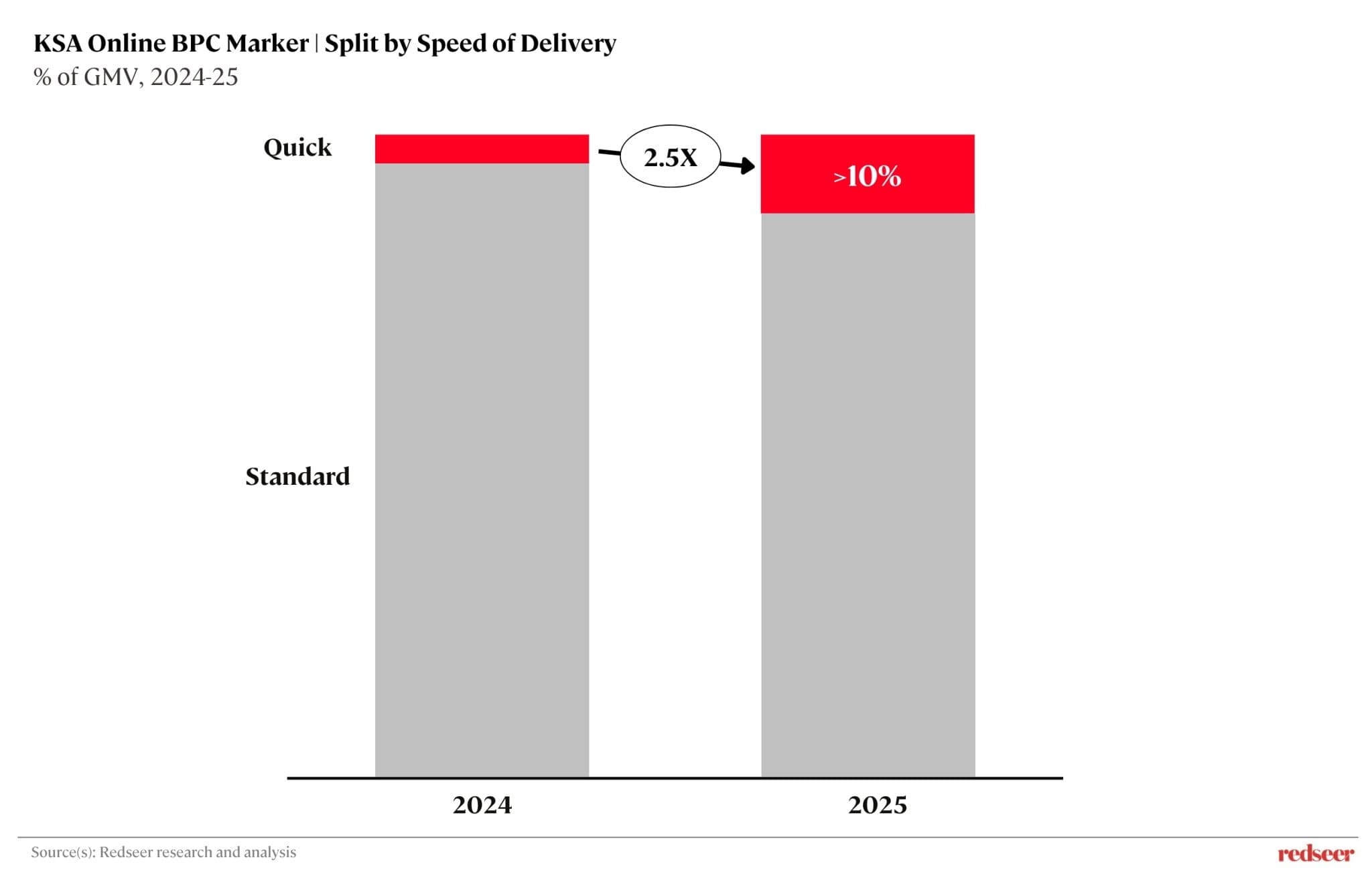

Quick delivery — defined as delivery within two hours- now accounts for clearly more than 10% of online BPC GMV in KSA. That number crossed the threshold in 2025, and it isn’t slowing down.

Why Beauty and Speed Are a Natural Fit

The first part of the story is intuitive. Personal care and everyday haircare are replenishment purchases – predictable, habitual, and low-deliberation. Quick delivery fits naturally: when you run out of a moisturizer or a shampoo, you want it today.

And the channel has attracted players across business models. Hyperlocals like Ninja have built their BPC proposition around exactly this. But omnichannel players have moved just as decisively – Nahdi launched “Nahdi Now”, a 30-minute delivery service rolled out across major cities, with online now contributing 25.8% of its total revenue, far exceeding the 12% target set just five years ago. Even pure-play e-tailers are adapting: Nice One delivered 40% of orders same-day in 2025, up from ~23% the year before – and while same-day doesn’t technically fall within the sub-2-hour quick bucket, it signals the same underlying shift. Speed is becoming a defensive play, not just a growth lever.

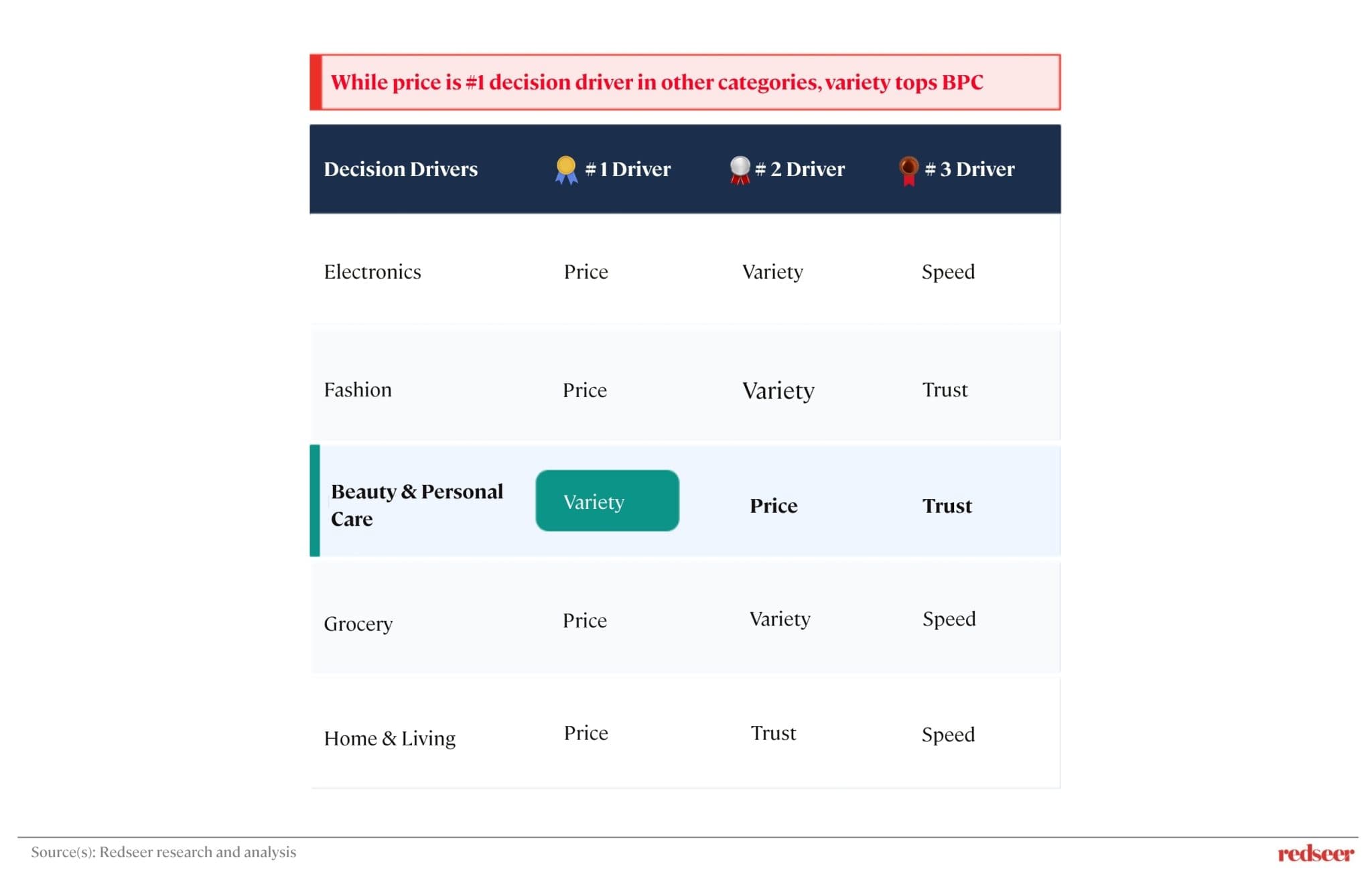

What’s more interesting, though, is what’s happening beyond the essentials. Unlike every other major retail category, the top purchase driver for BPC is not price; it’s variety. Consumers want access to a wider range, newer launches, and trending products. And increasingly, they want that variety delivered quickly too. That shift is showing up in basket data: makeup now accounts for roughly a quarter of quick BPC GMV – a meaningful share that signals this channel has moved well beyond the replenishment basket.

The Brands Being Left Behind

Here’s the uncomfortable implication: brands that aren’t available on quick channels are losing impulse and replenishment sales they may not even know they’re losing.

These aren’t big-ticket consideration purchases – they’re the reorder of a moisturiser, the top-up of a serum, the grab-and-go personal care item. When the consumer opens Ninja or Nahdi Now, and your product isn’t there, they don’t wait. They switch.

The channel is also evolving in another direction: platforms across the board are expanding private label portfolios in BPC, covering makeup, care, and fragrances, and the growth seen in private label in recent years is massive. These portfolios give platforms greater pricing flexibility, enabling competitive price points that raise the bar for branded players across the shelf.

For mass and mid-market brands, the implication is clear: being present isn’t enough. Being compelling, on assortment, on speed, and on brand equity is the new minimum.

The Brand Playbook for Quick Commerce

The brands navigating this well share a few traits.

They treat quick commerce as a distinct channel, not a delivery upgrade. Assortment for quick delivery isn’t the full catalogue; it’s the right SKUs for replenishment. Care-heavy, high-frequency, low-deliberation. Brands that map this correctly get a disproportionate share of the channel.

They invest in the trend cycle, not just the core range. Around 15–20% of online BPC GMV is driven by viral trends that reset annually. Korean beauty brands – COSRX, Beauty of Joseon, Some By Mi – are riding this cycle right now. These waves are real revenue, but they fade within 6–12 months. The brands and platforms that build infrastructure to onboard and amplify the next trend slot before competitors will structurally outperform.

They lean into what private label can’t replicate. Premium positioning, clinical credentialing, and brand heritage remain hard to imitate at scale. These are now commercial levers, not just marketing ones — and they matter more as platform assortments become more competitive.

The Platform Imperative

For platforms, the quick delivery arms race is intensifying. Sephora offers same-day. 6th Street delivers in 90 minutes. Centrepoint piloted quick delivery in Tier 2 cities. CBT players like Trendyol have set up local KSA warehouses specifically to close the speed gap against local players.

The bar is moving fast. Platforms that don’t credibly offer quick delivery for their core BPC assortment will increasingly cede the replenishment basket to those that do, and the replenishment basket is where customer lifetime value is built.

The Bottom Line

Quick commerce in KSA beauty isn’t a feature anymore. It’s a distribution channel with real GMV weight, structural growth tailwinds, and clear winners and losers already emerging. The two-hour window is where a growing share of beauty decisions are being made – not in a store, not after deliberation, but on a phone, in a moment, expecting near-instant fulfilment. Brands and platforms that have built for that moment are growing. Those that haven’t are losing volume they may be attributing to other causes.

Written by

Akshay Jayaprakasan

Associate Partner

Akshay brings over a decade of experience across consulting and technology, with deep exposure to India, Southeast Asia and the Middle East. He has delivered multiple keynotes, served on industry panels, and is frequently quoted by leading Middle East media on the digital economy.

Talk to me

Unlocking the Next Wave of MENA E-commerce Growth

The KSA Beauty Shelf Is Getting Crowded From Two Sides. Brand Equity Alone Won’t Hold It.

Omnichannel Owns a Big Slice of Online Retail in KSA

The Private Label Playbook is Moving from Retail Shelves to Dark Stores

‘Quick’ Emerging as a Growth lever for Online BPC in KSA

UAE Online Grocery: Dark Stores Have the Momentum. Retailers Still Have the Market.

Dark Stores Can Be Profitable. GCC Is Where It Happens First.

Three Consumer Shifts Shaping MENA’s Demand Landscape in 2025

KSA is the Online Fashion & BPC leader in GCC

Quick Retail Surges: Ninja Leads in KSA, Talabat and Noon Share the Lead in UAE

Value Retail: The Quiet Force Reshaping MENA’s Consumer Economy

Q-Commerce 2.0: Why Quick Retail is the New Norm- Quick Retail to be a bigger opportunity than Food delivery

Unlocking the Next Wave of MENA E-commerce Growth

The KSA Beauty Shelf Is Getting Crowded From Two Sides. Brand Equity Alone Won’t Hold It.

Omnichannel Owns a Big Slice of Online Retail in KSA

The Private Label Playbook is Moving from Retail Shelves to Dark Stores

‘Quick’ Emerging as a Growth lever for Online BPC in KSA

UAE Online Grocery: Dark Stores Have the Momentum. Retailers Still Have the Market.

Dark Stores Can Be Profitable. GCC Is Where It Happens First.

Related Redsights

Unlocking the Next Wave of MENA E-commerce Growth

The KSA Beauty Shelf Is Getting Crowded From Two Sides. Brand Equity Alone Won’t Hold It.

Omnichannel Owns a Big Slice of Online Retail in KSA

The Private Label Playbook is Moving from Retail Shelves to Dark Stores

‘Quick’ Emerging as a Growth lever for Online BPC in KSA

UAE Online Grocery: Dark Stores Have the Momentum. Retailers Still Have the Market.

Dark Stores Can Be Profitable. GCC Is Where It Happens First.

Three Consumer Shifts Shaping MENA’s Demand Landscape in 2025

KSA is the Online Fashion & BPC leader in GCC

Quick Retail Surges: Ninja Leads in KSA, Talabat and Noon Share the Lead in UAE

Value Retail: The Quiet Force Reshaping MENA’s Consumer Economy